If you were injured in an Amazon delivery accident in South Carolina, you are dealing with multiple insurance layers that insurers often try to limit to the smallest payout possible. This guide shows victims how DSP, Amazon, and underinsured motorist coverage actually work and why proving active delivery status is critical to unlocking full compensation. You’ll learn how insurers restrict claims, what evidence is needed, and how to identify every available source of recovery.

How Amazon Delivery Driver Insurance South Carolina Works Across Multiple Coverage Layers

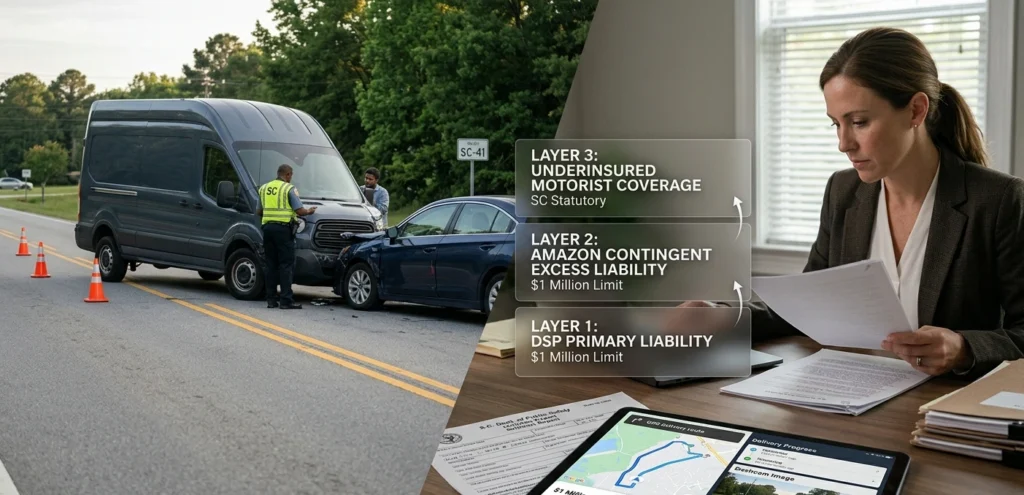

Amazon delivery driver insurance south carolina involves a layered system where Amazon contracts Delivery Service Partners (DSPs) to hire drivers and operate delivery vehicles under its brand, resulting in multiple insurance policies with different limits and triggers. After a crash, insurers often focus on the smallest applicable policy instead of disclosing the full scope of coverage available. Understanding the complete insurance structure early is critical to ensure all potential compensation sources are identified and pursued.

Layer 1: The DSP Company’s Commercial Auto Policy

The Delivery Service Partner (DSP) carries mandatory commercial auto insurance required by Amazon, which insurers often present as the primary or only coverage because it is easiest to access and sometimes has lower limits. These policies typically range from $300,000 to $1,000,000 and cover driver negligence during active Amazon deliveries. While valid, it is rarely the only applicable coverage and should not be the final source pursued.

Layer 2: Amazon’s Own Commercial Auto Program

Amazon’s commercial auto insurance covers DSP drivers while they are actively making deliveries, even though they are classified as DSP employees. Coverage applies only if the driver was on an Amazon delivery route at the time of the crash and can reach up to $1,000,000 per incident. Insurers often try to keep this policy out of claims involving unrepresented victims. Accessing it depends on proving active delivery status and correctly establishing that the coverage was triggered.

Layer 3: Amazon’s Direct Liability Coverage

Amazon’s commercial auto insurance covers DSP drivers during active Amazon deliveries, with limits up to $1,000,000 per incident, even though they are classified as DSP employees. Coverage applies only if the driver was on a delivery route at the time of the crash, which insurers often try to dispute to avoid higher payouts. Proving active delivery status is key to triggering this coverage and maximizing recovery.

When Underinsured Motorist Coverage Fills the Gap

South Carolina requires insurers to offer underinsured motorist (UIM) coverage, which applies when the at-fault driver’s insurance is not enough to cover your damages. In Amazon delivery cases, UIM may apply when DSP limits are too low, Amazon’s coverage is disputed, delivery status affects coverage, or multiple victims reduce available policy funds.

UIM is triggered through your own policy, not Amazon’s. Prompt notice to your insurer is required, and delays may jeopardize your ability to recover under this coverage.

What Amazon’s Insurer Does to Limit Your Coverage Access

Amazon’s claims team uses predictable tactics to limit payouts and reduce access to full coverage.

Common tactics include:

- DSP-only focus: Steering claims to the DSP policy and avoiding mention of Amazon’s coverage

- Delivery status disputes: Arguing the driver was not actively on an Amazon delivery at the time of the crash

- Early settlement pressure: Offering quick payouts before legal advice or full coverage review

- Amazon liability denial: Rejecting claims that Amazon’s systems or operations contributed to the crash

Recognizing these strategies helps protect your claim and ensures all coverage layers are properly considered.

How an Attorney Accesses Every Coverage Layer

Accessing all three insurance layers requires proving liability at each level with specific evidence, not just making a demand.

Coverage Requirements

- DSP policy: Proof the driver was on duty and negligent

- Amazon commercial auto: Proof of active Amazon delivery route at the time of the crash

- Amazon direct liability: Evidence of Amazon’s operational failure or oversight

Evidence Preservation

An attorney immediately sends legal hold letters to Amazon and the DSP to secure:

- App GPS and route data

- Driver safety scores

- Delivery activity logs

Without early preservation, key evidence may be lost and insurers control the narrative and coverage exposure.

Amazon Delivery Driver Insurance South Carolina Overview

Understanding amazon delivery driver insurance south carolina is important because coverage is layered across the DSP policy, Amazon’s commercial auto program, and potential direct liability claims. Insurers often try to limit payouts by focusing on the lowest policy or disputing whether an active delivery was taking place. Full recovery depends on proving coverage triggers using evidence like GPS data, delivery logs, and safety records, along with timely notice of your own underinsured motorist coverage. Early legal action helps ensure all available insurance layers are identified and pursued.

Do Not Let Amazon’s Insurer Decide What Coverage Applies to Your Case

Amazon’s insurer classifies your claim as soon as it is reported, which can limit the coverage applied if you are unrepresented. Thomas Conits at Spartan Law personally reviews each Amazon delivery accident case and pursues all available coverage layers from the start of representation.

Call 864-777-1000 now or visit the free consultation page to get started. No fee unless we win.

Frequently Asked Questions

1. Does Amazon’s insurance cover me if I was hit by an Amazon delivery van in South Carolina?

Yes. Amazon’s commercial auto program may cover DSP drivers during active deliveries up to $1,000,000 per incident. Coverage depends on proof the driver was on an Amazon delivery route at the time of the crash.

2. What if the DSP insurance is not enough?

If DSP limits are insufficient, Amazon’s policy and your underinsured motorist coverage may apply. An attorney helps identify and access each available layer.

3. How do I prove the driver was on an active delivery?

Amazon app GPS and route data show whether the driver was actively delivering. This evidence must be preserved quickly through legal action.

4. Can Amazon deny coverage?

Yes. Amazon may argue the driver was off-duty or finished deliveries. GPS and route logs are key to challenging that claim.

5. Should I notify my insurance company?

Yes. Prompt notice is required to preserve underinsured motorist coverage, but keep details brief until you speak with an attorney.

Key Takeaways

- Amazon delivery accident cases in South Carolina involve DSP coverage, Amazon’s $1,000,000 policy, and potential direct liability.

- Insurers often steer claims to the DSP policy to limit payouts.

- Amazon coverage depends on proof of active delivery via GPS or route data.

- Underinsured motorist coverage may apply if damages exceed limits, with timely notice required.

- App data and dashcam footage may be lost within 24 to 72 hours.

- Early legal help is critical to protect coverage and evidence.